set up trust

Protect your assets and benefit your family

Guide for Trust

Trust is a legal structure used to achieve unique ownership -- Trust rights and interests.

Trust can be used for protecting private assets, to insulate against risks, to fulfil the wishes of individuals and organisations, and also for specific tax and financial arrangements.

TRUST KNOWLEDGE

A trust is a legal structure, bypath a specific legal process. Settlor set up a legal structure (and appoint a Trustee) to take the title of and allocate the assets which once held by the Settlor. The transfer of assets owned by a private individual (Settlor of the trust) to the trust could result in a legal separation of the property's ownership from the Settlor,and could avoid any uncertainties such as marriage, death, litigation, debt and taxes, which may incur impact or loss in the future, by which such property shall be adequately protected. In short, such behaviour as the Settlor entrust his/her assets to a Trustee on his/her specific purpose, and its corresponding legal structure, are what we call trust.

A trust is a virtual entity established by a Settlor. Such entity shall be protected by law and consisted by the Trustee(s) and a Trust Deed which shall be strictly executed by the Trustee, and the Trustee instead of the Settlor shall exercise possession of the assets and take the title of the rights and interests. - The New Zealand law states that trust is not an entity like a corporation, but an obligation affiliated with a Trustee. - Such virtual entity exercises its power on the assets held by the trust strictly according to the Trust Deed as well as the Trust Memorandum and distributes the pre-defined interest to the Beneficiaries designated in the Trust Deed.

As a specific legal structure and ownership management tool, a trust can adequately protect the Settlor's interests and assets. Trust can be used for safeguarding private assets, to insulate against risks, to fulfil the wishes of individuals and organisations, and also for specific tax and financial arrangements.

In the meantime, trusts could also be used for investment, property separation, inheritance, charity, tax planning, or for the avoidance of contingent judicial claims.

YES. The trust is a legal structure and tool which has a long history in Commonwealth countries and its practicality has been testified and proved by hundreds of years of legal practice. It is no exaggeration to say that the concept of trust and the Acts and Law of Trust shall be part of the fundamental and origins of Common Law. In New Zealand, where a large number of British laws have been inherited, the Act of Trust is one of the fundamental Acts of New Zealand's legal system. The rights and interests of the trust are legally recognised and strictly protected.

The Trust originated from its predecessor USE in ancient Europe, as the Knight who was about to go to the battlefield (Feoffor to USE) entrusted his property to the person whom he trusts (Fees to USE) to support and protect his families and offspring. In the thirteenth century, USE was firstly used by England's clergy to counteract the Church's ban on holding property, gradually such behaviour had been accepted by aristocrats and the general public, and used against the monarchy and feudal burdens. In the late 14th century, almost all of the land was held by USE in England. In 1535, King Henry VIII promulgated the "Statute of Uses", the" Positive USE", which was allowed by such law, and was gradually evolved into today's trust. In 1893, Britain issued the first trust law "The Act of Trustees", which defined the trust rights and interests of modern legal significance. As one of the legacies of the Magna Carta, trust rights and interests are recognised as inviolable "private property rights" and are inherited and protected by subsequent laws and regulations of trust.

The Trust Act is one of the cornerstones of New Zealand's legal system. New Zealand's trust law comes from England. The current trust law is the Trust Act 1956 / The Trustee Act 1956, which is the revision and re-enactment of the Trusts Act 1908.

The New Zealand Law Commission started to amend the Act of Trust 1956, which has been in place for nearly 60 years, in 2009 and submitted to Parliament in late 2016. The new “Trusts Act for New Zealand” draft is being discussed and tested and will come into effect soon.

Compare with other countries, in New Zealand trusts take a more critical role in the society and the economy. It’s estimated that there exist around 300,000 to 500,000 Trusts in New Zealand. Due to abundant legal practice, terms of New Zealand's trust law are introduced by many other Commonwealth countries or regions, such as Hong Kong, Jersey, BVI, etc.

The uniqueness of New Zealand Trust Law resides in the flexibility of the Trustee's role in a trust structure. In many other countries and regions, trust laws provide that a Trustee shall be solely entrusted with the custody of assets, take charge of management and investment, and distribute and relocate of assets. While the New Zealand Law allows the obligations of a trust, such as custody of Trust Asset, investment managing, consulting, even the entire trust administration, to split into independent obligations, and then to entrust different agencies or individuals to take charge. For example:

- New Zealand resident and legal entity could be appointed as a custodian Trustee (principal Trustee), and entrusted with the custody of the Trust Fund;

- The Settlor may appoint a Swiss investment company as an investment management Trustee to manage the investment of the Trust Assets;

- The Settlor may also appoint a trustworthy family counsellor as a consultant Trustee to supervise the operation of the trust.

- The Settlor may else designate a professional with senior management experience as a management Trustee to take charge of the trust maintenance and administration job.

- Also, New Zealand's law has introduced a role called Advisory Trustee to enable Settlor to participate into the management of the trust legally, while guaranteeing the trust to be insulated from the juristic claim and ensure the effectiveness of tax planning. Such a role is a realistic judicial practice for Settlors who want to "control" the trust property and hope such “control” will not impact on the trust's legality simultaneously. After conducting the asset management activities regarding the opinions of the advisory Trustee, the other Trustee shall not be liable for the profit and loss of the Trust Assets. All trust management activities, excluding the discretionary power to the Beneficiaries, shall follow the instructions of the advisory Trustee. Such a role is usually assumed by a donor of the Trust Asset where usually the donor is the Settlor.

Another feature of New Zealand's trust law is the law does not recognise "trust" as a "legal entity" as a company but as specific obligations and rights of the Trustee which originated from Trust Deed. In contrast, including the OECD's CRS procedure, laws in most countries of the world consider trust as a "legal entity". Therefore, any trust established in New Zealand will be recognised as a non-investment entity (NFE) as long as the Trustee is not a financial institution or a professional Private Trust Company (PTC), and the trust holds no passive investment instruments or financial assets; such conditions will not meet the CRS " Investment Entity " test (see Standard for Automatic Exchange of Financial Account Information in Tax Matters, Section VIII, A / 6, a & b) thus not require compliance with CRS compliance obligations. In 2016, the New Zealand Inland Revenue requires overseas trusts (Settlor is not a New Zealand Citizen or a permanent resident) established in New Zealand to report Trust Elements to the IRD (with IR607 when setting up and IR900 for annual declaration) from 2017, which is a transparent procedure to the IRD but not a CRS submission.

It should be noticed that in some countries, the concept of "trust" has become controversial and trusts/trust companies have become an investment vehicle and specialised investment financial institution. This is only an application scenario of the concept of trust; such narrow sense should not be used to define the trust and mention making an understanding of trust under Common Law.

The Trustees take the title of the Trust Fund and execute such assets according to the Trust Deed and the Trust Memorandum which entrust them to manage the Trust Assets. The Beneficiaries enjoy the income or profit distribution of the Trust Assets by the Trustees' discretion which empowered by the Trust Deed.

No. Once the Settlor has transferred the asset to the trust, the Settlor no longer takes the title of such assets according to the law, nor should regard and conduct himself/herself as the owner of such assets, even if the Settlor may also be the Trustee and/or Beneficiaries at the same time. Settlor shall strictly comply with the Trust Deed while exercising any rights and obligations, including to deal with the Trust Fund (Trust Property).

Businessman and professionals such as lawyers, accountants, etc., whose activities might incur contingent risks but without limited liability, may choose to transfer their assets into a trust to isolate contingent risks.

For high-net-worth individuals, we recommend to set up a trust to protect their private property, considering uncertainty disputes that may arise as a result of inheritance or distribution real estate, and the indefinite impact on private property that might incur by tax planning and operational liability.

Entrepreneurs, who wish their business, organisation, equity, rights, and interests held by individuals to be continued retaining their original purpose and constitutions after their death or loss of legal capacity. Then, it is a wise choice to transfer the ownership of their enterprise, organisation, equity, rights, and interests to a trust that operates strictly complying with a Trust Deed to fulfil their wishes.

Property Owners who live in such nations with laws unsound, where private properties (refers to funds, shares, securities, precious metals, equity, intellectual property, copyright and other movable property) might be deprived unlawfully, shall achieve protection by transferring their assets to a trust established in a nation where private properties shall be ruled by law and protects private property lawfully. Such properties shall become a Trust Fund and be treated and protected from being deprived as private property owned by the residents or entities of such country.

Placing assets in trusts shall be able to protect the assets against third parties (individuals, institutions, even governments) by the fact that such assets have been legally not owned by the Settlor anymore.

To transfer the assets into a trust shall protect the integrity of the assets such as a company from the affection of the consequence of inheritance, marriage and other relationships. Under the protection of a trust, the integrity of the assets and decentralised interests for the Beneficiaries are no longer opposites.

To place assets in a trust can be employed to lock in the business intentions, principles and purpose of an enterprise and organisation. No matter what happens, such principles and purpose shall be strictly observed and enforced by the trust complying with the Trust Deed and the Trust Memorandum* till the end of the Trust's Vesting Day.

The placement of assets in trusts has also been used to guarantee the property, in most cases, a business or a specific interest, to receive national treatment from the country where the Trustee is located and enjoy the same tax and judicial benefits as the nationals of such country for certain tax and legal planning purposes.

Not for sure. In some cases, if the litigant is also a Settlor, a Beneficiary, or under a marriage (including cohabitation) with the Settlor, there exists New Zealand Law ( RPA Act) allowing such litigant to proceed actions on their assignable portion of the Trust Fund.

Besides, if the authorities have found any evidence indicating that the assets have not been legally delivered into the trust (e.g., the Settlor manipulates the Trust Assets without the Trustee's consent, which in violation of the Trust Deed), like a false trust, the law shall support the litigant’s juristic claim and action on such Trust Property. If there is evidence indicating that the trust is controlled by the Settlor, for instance, the Settlor, the Trustee, and the Beneficiary are highly overlapped, such trust shall be judged as a false trust and lose the protection of the law.

Also, if there is no specific preventive arrangement in the Trust Deed, the Beneficiaries, after being sued, might have some or all of the "assigned assets that to be distributed from the trust" to be claimed and deprived by the support of the court.

Finally, if the Settlor has been already insolvent when transferring his/her assets to the trust, the claim shall be supported by New Zealand law as long as the obligee has evidenced that the Settlor's conduct is "evade debt maliciously", and such transferring will be sentenced invalid.

To protect the Trust Fund from being claimed, we recommend our clients to transfer their assets into trusts and designate suitable third-party Beneficiaries, such as lineal descendants, the Settlor's disability insurance and pension insurance, or third-party funds, e.g. education funds for descendants, charitable funds, etc., before any litigant claims on such assets, and assesses indicates there are contingent risks.

In New Zealand's legal practice, the assets that have been transferred to a trust/Trustee for more than three years as of the time of the Settlor's insolvency shall be in great probability presumed to be the Trust Fund and protected, unless the litigant could provide even more solid evidence against that.

Trust Assets shall not become part of the legacy, and the Trust Fund shall still be maintained and distributed complying with the Trust Deed and Trust Memorandum.

As a universal situation, in a trust, the Trustee follows the Trust Deed to distribute the trust's income and interest to the Beneficiaries of the trust. If there is no specific stipulation in such deed, for example, if the Trust Fund has become insufficient to distribute; if the Trustee needs to be changed when the Settlor has died or lost civil capacity; if the Beneficiaries have also passed away or lost their capacity for civil conduct, the mentioned Trust Memorandum shall be followed, the circumstances shall be assessed complying with the memorandum's principles, and the appropriate action shall be decided.

According to New Zealand law, the maximum duration of trust is 80 years, and the coming soon new act expands such period up to 125 years. When any person transfers his/her asset that is legally achieved into a newly created trust, the ownership of the asset changes immediately, and the ownership shall remain unchanged throughout the next 80 (125) years, even if the Settlor passed away. Of course, Settlor can set a desired trust Vesting Day not exceeding the limits mentioned above.

In New Zealand, which nation was founded upon the treaty of Waitangi, the legislation not only emphasises protecting private property but also has predictability. The stability of the legal system of a country is an essential consideration for those trusts that need to survive for a long period, and New Zealand has a unique advantage over the rest of the world in this regard. New Zealand has a long history and well-established laws of trust. The longest surviving trust in the world today exists in New Zealand. As private property, the Trust Fund (Assets held by the trust) is well protected by New Zealand law. Thereby trusts are pervasive in the nation's economy, and the cost of establishing trust and the subsequent administration is relatively affordable.

It is noteworthy that New Zealand law allows foreigners to set up private trusts in New Zealand for up to 80 years, (and the coming soon new trust act to be implemented increased such period till 125 years), and protects the oversea Trust Assets on a par with New Zealand citizens.

Considering the legal environment and tax planning, New Zealand's unique sovereignty structure (the Cook Islands and Niue are sovereign states with free association with New Zealand, and economy linked with a series of Commonwealth countries in the Pacific region), provide enough flexibility and probability for building various trusts and legal structures to meet the diverse needs of clients from all over the world.

In addition, in case there is a potential dispute over the Trust Deed, aside from the New Zealand Supreme Court, litigants can take advantage of the Cook Islands‘ jurisdiction and appeal to the Judicial Committee of the Privy Council (United Kingdom) as the Court of Final Appeal, thereby be availed the Equity law. Equity is world widely recognised as the fairest and effective legislation to resolve international commercial disputes. Its unique remedies, such as using specific performance to enforce the Deed fulfilled by litigants as equitable remedies, have important practical significance for protecting the Innocents against breaches of trust.

HOW TO SET UP A TRUST

-

![]()

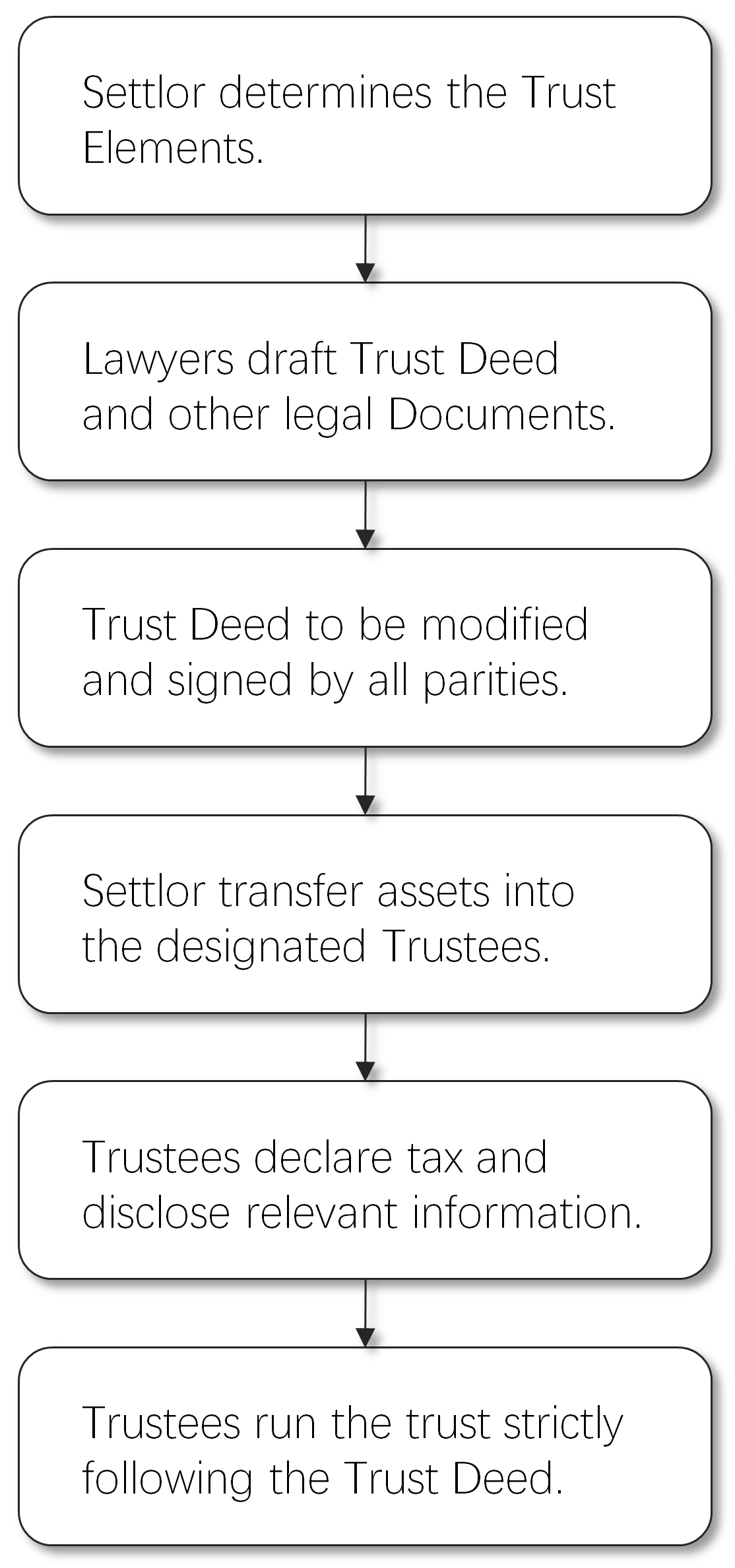

The Process of Setting up a Trust

- The client / Settlor determines the Trust Elements.

- Our lawyers draft the "Trust Deed" and other relevant legal documents according to above trust elements.

- The "Trust Deed" shall be modified until all parties have agreed on and complied with it (under the legal premise). Such Trust Deed shall be signed by all parties including the Settlor and the Trustees under witness.

- Complying with the Trust Deed, the Settlor shall transfer the assets to the Trustee designated by the Trust Deed.

- The Trustees declare tax and disclose the statutorily required information of the (oversea) trust to authorities.

- The Trustee shall complete the stipulations of the Trust related matters according to the Trust Deed, including but not limited to the distribution of Trust Fund and revenue, routine administration and accounting, an audit of the Trust Fund, tax declaration and payment annually, compliance the major trust issues, etc.

-

Trust Elements

Settlor: the person or entity establishing a trust is called the "Settlor". The Settlor is usually the initial owner of the assets held by the trust (see "Trust Fund" below, such as the Settlor's house and any other assets).

Trustee: a Trustee is a person or an entity who holds and manages the Trust Fund. In general, the Trustee must be legal persons/entities, at least one person/entity is chosen as a Trustee, and the Settlor may be one of the Trustees (at least two or the trust shall fail). To appoint an independent Trustee, who is not the Settlor, not a company controlled by the Settlor, and not a Beneficiary, is a wise choice to avoid legal risks.

Trustees shall hold the Trust Fund. New Zealand laws provide that a trust is not a legal entity and the Trust Fund shall be held by a Trustee, while in many other countries the assets shall be held by a "trust" which is considered as a legal entity, and the Trustees only take responsibility of managing the trust. Trustees may decide to distribute any Trust Fund to any particular Beneficiary or not. The Trustee must ensure that the Trust Deed shall fulfil the Settlor's wishes. It is also the responsibility of the Trustees to take into account the interests of the Beneficiaries in each of their decision.

Beneficiaries: the persons or entities who may benefit from the trust are called Beneficiaries. In a Family Trust or Private Trust, the Beneficiaries are usually members of the family, including possible future members such as unborn grandchildren. Beneficiaries are generally divided into two groups:

- Discretionary Beneficiaries: Discretionary Beneficiaries shall be the persons/entities who can benefit from the trust. The Trustees are free to determine whether a Beneficiary could receive any benefit from the Trust.

- Final Beneficiary: The Final Beneficiary shall be the persons/entities who are likely to receive whatever assets have been left in the Trust when the Trust is wound up.

Trust Fund: A trust must have some assets in existence. When establishing a trust, the Settlor can transfer the assets to the trust. Such assets and generated interests in the future comprise of the Trust Fund. According to the Trust Deed, the Trustees shall under the obligations to the custodian, maintain and distributes such assets.

Once a trust has been established, the Settlor shall transfer his/her assets into the trust with a minimum of NZD $10. The assets shall be transferred gradually or once in all into the trust by way of gift or loan.

Vesting Day (expiry date): Generally, trust has a maximum life of 80 years (125 years according to the coming soon new law), although many trusts are wound up earlier than that.

Trust Deed: The establishment of trust requires a set of legal documents which form a complete Trust Deed so that the trust can be established and run under such deed. The Trust Deed sets out the Settlors’ wishes about how the Trust shall be run and who shall benefit from the assets held by the Trust. Trust Deed also defines the rights and obligations of the Trustees; the Trustees must follow the Trust Deed when operating and performing of each trust issue.

-

Cautions

When setting up and managing your trust, be sure to get a lawyer's advice.

If your trust is not properly established or managed, there may arise risks like disposing of the Trust Fund in an unwanted manner of the Settlor, or the trust disables to provide the desired protection.

Please keep strictly complying with the Trust Deed during the Trust Period.

Do not violate the Trust Deed. For instance, the Settlor disposes of the Trust Property on his/her own without the consent of Trustees or the Beneficiaries mortgage their designated share of the Trust Fund in any way. Such behaviours can lead to a series of legal consequences such as the failure of the trust or the Trust Fund which once protected by the law, and then incurs inestimable consequences such as generating an unexpected tax burden or the contingent juristic claim and deprivation of the Trust Fund.

-

Overseas Trusts / Offshore Trusts

Under the laws of New Zealand, trusts established in New Zealand by non-New Zealand citizens or permanent residents as Settlors are recognised as overseas trusts (or offshore trusts).

Overseas trusts have the same rights and obligations as trusts established by New Zealand citizens, exceptions as below:

The trust elements must be disclosed to the New Zealand tax authorities (IRD)

Income from overseas (out of New Zealand) of the trust is exempt from income tax of New Zealand.

Revenue arising within New Zealand shall be taxed based on income tax rules as New Zealand tax resident follows.

Revenue arising within New Zealand, under distribution to Beneficiaries of non-New Zealand residents, shall be taxed based on the withholding tax rules of New Zealand.

-

Gold Trust

Our Gold Trust is a type of bare trust. A bare trust is a simple trust structure that is used only to hold a single asset. The Trust Property is not distributed and paid to beneficiaries during the existence of the trust.

This kind of trust is relatively simple since the unique trust structure, while the rights and obligations of the Trust Deed are relatively concise. Compared with other complex structure trusts, the legal cost of opening and maintaining a Gold Trust shall be much cheaper.

Also, the Trust Assets of Gold Trusts do not generate revenue and profits and do not require annual audits and valuations.

It is relatively simple for a Gold Trust to report to the taxation department every year.

The Bare Trust structure is suitable for most people to protect the property rights and usufruct of their real estate, as well as for the protection of the ownership and usufruct of their stored gold.

-

Costs and Pricing

As a rigorous legal instrument that needs to be strictly implemented, the main cost of setting up a trust is legal works. The more complex of the trust structure is, the more professionals and lawyers required and the higher the cost increases. In particular, to establish a trust with complex overseas properties, such cross-border issue requires lawyers, accountants, authenticators and other professionals /teams from different countries to perform their duties and cooperate with each other. Generally, pricing shall be based on total working hours. An ordinary Australian lawyer's charge shall be around $400 AUD/hour, $1,000 - $2,000 AUD for a senior solicitor from law firms with good reputation while the charges from partners' shall be even higher. Establishing a composite cross-border trust costs tens of thousands to millions of dollars is not rare cases. In addition, trust needs to be maintained annually. Major maintenance costs come from the auditing, as well as tax returns and legal cost for compliance with matters carried out by the Trustees.

Compared with the above mentioned, bare trust has a compact structure, which holds a single type of asset, no need for auditing annually. Most lawyers shall be able to accomplish such work in one or two days, and the cost of setting up as cheap as not exceeding $3,000 AUD. We recommend our clients without any intent to distribute wealth to the Beneficiaries as well as clients with no business use of the trust, to adopt such bare trust to hold their assets.

Please find our quotations as shown in the below table, where the quotations include 15% GST but not include the cost of add-on features of trusts:

Unit(AUD) GPN Trust Gold Trust Gold Trading Trust Gold Trust/GPN Trust VIP Private Trust 2,300 2,450 3,600 3,600 By Enquired Set up Trust 1,500 Open Bank Account N/A 500 N/A Legal Documents 650 1,000 Time Basis Charge Trust Maintenance(1st year) 150 600 2% Trust Maintenance(Fr 2nd year) 150(Free: Transaction 4+/PA) 150 500 500 By Enquired from 1.2% Deposit-able in Cash N/A NO "Sure Thing" Initial Trust Fund Not Required 500 oz 1 Million oz Trustee Gold Intrust(NZ) Gold Intrust NZ / Solicitors appointed by Gold Intrust NZ Solicitors/Legal Firms appointed by Settlor(changeable,changing fee charged) Advisory Trustee Individuals designated by Clients(unchangeable) Individuals designated by Clients(changeable) Beneficiaries Individuals designated by Clients(unchangeable) Individuals designated by Clients(changeable) Settlor Individual Individual/ Offshore company and Business entity in BVI / Cayman / Hong Kong / Singapore Investment management Trustee No Designated by Clients Privacy Firewall Gold Intrust Swiss (optional) Designated by Clients Max Trust Period 80 years Trust Fund GPN Gold Gold + Deposit Gold + Deposit + GPN Gold + Deposit + GPN + Other Properties

Start to Set up a Trust

For the security and compliance reasons, in order to access the online system to customize a trust

we kindly invite you to submit and verify your identity.

Before using the system, please read carefully and understand the knowledge

and cautions of trust described above,

so as to prevent inconvenience caused by an incorrect setting.

We appreciate your understanding and cooperation.